Debt consolidation is a term many people search for when they are overwhelmed by multiple payments, high interest rates, or the emotional stress of mounting financial obligations. It is often presented as a clean, simple solution to combine all your debts and pay less every month.

For consumers with credit card debt, this can work. But when it comes to business debt, particularly high-cost obligations like Merchant Cash Advances (MCAs), debt consolidation takes a very different form known as Reverse Consolidation.

If you are a business owner considering a reverse consolidation to manage your daily or weekly payments, it is critical to understand exactly how it works, why the math often works against you, and what your better alternatives are.

What Is MCA Reverse Consolidation?

Because traditional bank loans and debt consolidation products are rarely available for MCA debt, lenders in this space offer a product called reverse consolidation. It is marketed as a lifeline for businesses with multiple merchant cash advance payments, but it is fundamentally different from a standard loan.

How It Works

In a reverse consolidation, a lender provides a funding agreement not meant to pay off existing debts, but rather to help lower near-term daily payments.

- The Mechanism: The new lender pays a portion of the weekly or daily payments to existing MCA providers on your behalf.

- The Exchange: In return, they collect one payment from you (typically lower than your current total daily draw) over a longer term.

On the surface, this sounds like relief because your daily cash flow improves immediately. However, the underlying reality is often much harsher.

- You are still responsible for 100% of your original MCA balances.

- You are adding a new debt (often with a high factor rate) on top of existing obligations.

- You are prolonging the debt, often resulting in paying significantly more in total fees.

The Hidden Math: A Real-World Example

Understanding "Positions" and the Long-Term Cost

In the MCA space, a "position" refers to an individual funding agreement. Business owners often end up accumulating multiple positions from different lenders, and they each have a priority for who gets paid back first.

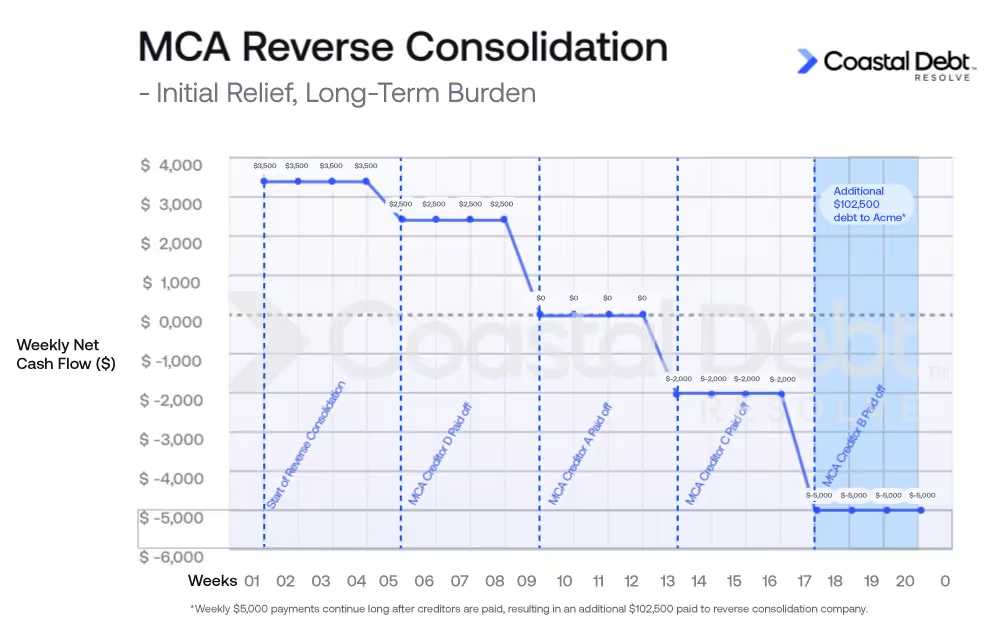

To illustrate why reverse consolidation can be dangerous, let’s look at a hypothetical scenario.Â

The Scenario

A business owner has 4 existing MCA positions and is struggling to keep up with the payments.

- Creditor A: $50,000 balance (pays $2,500/week)

- Creditor B: $80,000 balance (pays $3,000/week)

- Creditor C: $25,000 balance (pays $1,000/week)

- Creditor D: $50,000 balance (pays $2,000/week)

Current Situation:

- Total Debt Owed: $205,000

- Total Weekly Payments: $8,500

The Reverse Consolidation Offer

A lender ("Acme Funding") offers to cover the $8,500 weekly payments. In exchange, the client agrees to pay Acme $5,000 per week until the new total balance is paid off. Acme charges a 1.5 factor rate on the total debt they are managing.

- New Total Debt: $205,000 x 1.5 = $307,500

Why the Math Doesn’t Work

The client feels relief because their weekly payments dropped from $8,500 to $5,000. However, look at what happens as the original creditors are paid off by the reverse consolidation company.

- Creditor C is Paid Off: Acme’s payments drop by $1,000/week. The client still pays Acme $5,000/week. The client’s weekly savings drop from $3,500 to $2,500.

- Creditor A is Paid Off: Acme’s weekly payments drop by another $2,500. The client still pays Acme $5,000/week. The client is not saving any money per week.

- Creditor D is Paid Off: Acme now only pays out $3,000/week for Creditor B. The client still pays Acme $5,000/week. The client would have been saving $2,000 per week.

- All Creditors Paid Off: Acme pays out $0/weekly. The client continues paying $5,000/week until the full $307,500 is satisfied.

The Final Result

- Initial Debt: $205,000

- The Cost of Reverse Consolidation Cash Flow Relief: $102,500

- Final Amount Paid: $307,500

The business owner paid an additional $102,500 in fees on top of the original debt for reverse consolidation cash-flow relief. This structure creates temporary breathing room but often guarantees a long-term financial loss.

Reverse Consolidation vs. MCA Debt Relief

If reverse consolidation is merely delaying payments at a high cost, what is the alternative?

MCA debt relief is a fundamentally different approach. Unlike consolidation, which simply moves debt around, relief aims to provide cash-flow relief and reduce the total amount owed.

Is Debt Consolidation Right for You?

It is vital to choose the financial tool that aligns with your reality.

- For Consumers: If you have high-interest credit card debt and a good credit score, a traditional consolidation loan from a bank could work well for you.

- For Businesses with MCAs: If you’ve accumulated multiple cash advances, relief is often the only path that addresses the root problem without adding a lot of new debt.

Ready to Re-write Your Financial Story?

Don't let short-term relief turn into a long-term burden. MCA Debt Repair assists qualifying small business owners in negotiating MCA debt obligations to help you regain control of your revenue.

Disclosures: MCA Debt Repair assists businesses in negotiating and settling certain commercial obligations. We are not a lender and do not provide legal, tax, financial advisory, or credit repair services. Program terms, savings, and timelines vary by client, creditor participation, contract terms, and the client’s ability to save. Individual results will differ. Services are not available in all states and are not intended for consumer or personal debt. This content is for informational purposes only and should not be relied on as legal or financial advice. You should consult with your own professional advisors regarding your specific situation.